Sunday, May 5, 2024

Once Governor Inslee signs House Bill 1474 into law, effective January 1, 2024, the cost of recording real estate documents will increase by $100 per document to $304.50. Two years ago the cost was $104.50, so this fee will now have been increased $200, or 195% over two and half years.

In a typical financed home purchase, three documents need to be recorded separately. The Deed, the Deed of Trust securing a new mortgage loan to the property, and the Reconveyance of the Seller’s former loan secured to the property. The costs related to a standard home purchase will now increase by $300 at the beginning of 2024. What was formally a transaction cost of $304.50 on a typical home purchase is now going to be $913.50. It doesn’t matter if the cost of the home is $5,000,000 or $250,000. Truly, the increase will harm the lower end of the housing market more so than the upper end.

The $100 increase two years ago was to cover costs related to homelessness. The new increase will fund a program regarding race discrimination in the housing market. The text of the bill can be found here: 1474-S2.PL.pdf (wa.gov).

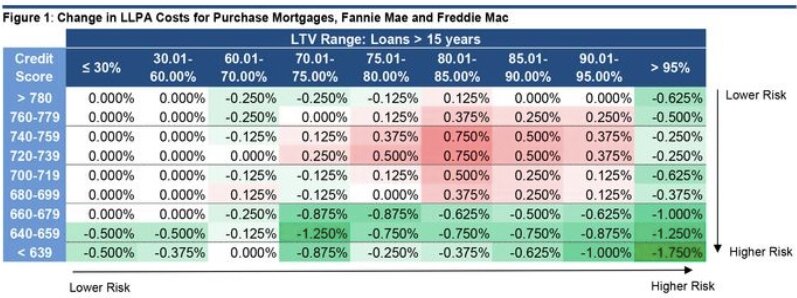

In other news the Federal Housing Finance Agency has changed their risk pricing structure via Loan Level Price Adjustments. In general, the changes increase fees on borrowers with higher credit scores and reduce the fees on borrowers with lower credit scores. The changes can be seen on the table below which the Wall Street Journal obtained from Evercore ISI Research and published.

These are only changes to the rates, not the actual rates. Those home buyers making a down payment of 20% with a credit score of 720-759 will face the greatest increase in fees. Lower credit score borrowers are still paying higher rates than higher credit score borrowers, as they should since they pose a greater risk of default. If you want to review the current rates or the prior rates, you can visit the FHFA website at fanniemae.com.

Flip to your favorite cable news channel and you can hear about which groups are helped/ harmed by these changes. While they focus on that, what they aren’t focused on are the real-world impacts of these changes.

First, as reported by the Wall Street Journal, citing the American Enterprise Institute

“default rates of Fannie/Freddie owner-occupied 30-year fixed rate purchase loans acquired in 2006-2007 and found that among borrowers with credit scores between 720 and 769 and 20% down payments, the default rate was between 4.2% and 8.8%. Among borrowers with less than 4% down payments and credit scores between 620 and 639, the default rate was between 39.3% and 56.2%”

In summary, the riskiest borrowers are 6-10 times more likely to default than the least risky borrowers on the schedule above, depending on the down payment amount and credit score. However, if you look at the current rates now being charged, the fees for the higher risk borrowers in the ranges cited in the Wall Street Journal quote above, are only 3.5 times greater. The risk vs. the risk premium being charged doesn’t jive, which is why the Wall Street Journal referred to this as a form of “socialized mortgage lending risk”.

Interest rates have risen, the Federal Reserve is on a mission to increase unemployment, a recession is on the horizon. Is now the best time to provide incentives to borrowers that are a greater risk? What does a neighborhood look like when there are unoccupied homes that have been foreclosed?

As reported by the Wall Street Journal on May 8, effective May 31, the Department of Energy will implement standards on the Manufacture Home Industry that will add a cost of $4,500 to the cost of a new manufactured home. The purpose is to reduce their carbon footprint by the year 2050. The median household income of Americans that live in these homes is $35,000 per year. Manufactured homes comprised 9% of new single-family home starts in 2021, providing 100,000 affordable homes.

The Wall Street Journal further states that manufactured homes already have a relatively small carbon footprint. Yet, as Senator Tim Scott recently noted in a letter to DOE Secretary Jennifer Granholm, the low income purchasers of these homes are being “unfairly asked to bear the costs imposed by climate alarmists”.

The system of affordable home ownership is becoming more and more disjointed at the wrong time.

Comments

No comments on this item Please log in to comment by clicking here